By Brian Massie, A Watchman on the Wall

Thanks to a Lake County lobbyist for sending us this timely article dealing with Ohio’s property taxes. We have inserted our comments throughout the article.

Please remember: “Any tax that, if unpaid, causes a citizen to become homeless is immoral.”

Joint Committee on Property Tax Review and Reform continues hearings

Written on Mar 1, 2024

By Hannah News Service

A veteran of Ohio tax administration told the General Assembly’s property tax study panel Wednesday that the flagship policy for preventing spikes in tax bills no longer works well.

The Joint Committee on Property Tax Review and Reform hearing included testimony provided by experts at Zaino Hall & Farin, including former Ohio Department of Taxation (ODT) Commissioner Tom Zaino, former Senate majority budget director Brian Perera and tax attorney Stephen Hall, former ODT assistant counsel.

Zaino said that HB920 of the 111th General Assembly, enacted in 1976 to prevent large run-ups in property values from driving proportionate property tax increases, isn’t achieving its intended purpose anymore because of school districts’ ability to seek voted millage not subject to HB920 limitations.

“Based on research and available data, we believe school districts have done their own type of ‘tax planning’ by utilizing levies that have been enacted over the last 48 years but which are exempt from HB920. As a result, HB920 is broken. We will show why HB920 is broken and why it no longer works to protect Ohioans from inflationary increases in property taxes,” Zaino said.

Of the 333 school districts that were at the 20 mill floor in 2022, 264 or nearly 80 percent had millage not subject to HB920.

Zaino described how the allowed purposes of emergency levies not subject to HB920 had expanded over the years, from providing for emergency requirements and preventing school closings, to include avoiding an operating deficit, among other changes.

“I suggest that all general levies are intended to avoid an operating deficit,” Zaino said.

“Since at least 1994, emergency levies appear to now be routine and no longer indicate a true state of emergency,” he said.

“It needs to be strengthened to achieve its intended purpose,” Zaino said of HB920.

Zaino also said Ohio’s property tax system does not achieve one of the key characteristics of an optimal system – simplicity.

The witnesses outlined a few potential fixes for Ohio’s property tax system.

– Fixing HB920 by factoring emergency and substitute levies and school district income taxes into determinations of whether a district is at the 20-mill floor.

– Renaming emergency and substitute levies so taxpayers truly understand them, and limiting emergency levies to true emergencies.

– Smoothing out the valuation process with more frequent revaluations or revaluations in portions of counties.

– Addressing the difficulties faced by those unable to pay inflating property tax bills, such as through the use of enhanced homestead credits, income-based circuit breakers, property tax deferral programs and monthly payment of real property taxes.

Zaino said in some ways not much has changed since he chaired the Taft-era Committee to Study State and Local Taxes. Among the 39 recommendations from that effort was “establish a special committee to examine the real property tax.”

In addition, Zaino said because the committee is charged with reviewing “all aspects” of property taxes, it should also look at taxation of tangible personal property. He said Ohio has uncompetitive tangible personal property taxes on utility properties, which are subject to taxation on up to 88 percent of their assessed value, compared to 35 percent for homes.

“These high listing percentages are an obstacle for Ohio-based investment in the infrastructure maintained by these public utilities. If new investment is made in Ohio infrastructure, then the cost of doing business in Ohio, or living in Ohio, is increased,” he said.

While responding to questions from Sen. Louis Blessing (R-Cincinnati), Zaino said he does not think state valuation procedures are causing the problem.

“I know that some folks point to, for instance, the Department of Taxation’s not doing the right job when it comes to valuation … I fight, I sue the Ohio Department Taxation every day, but I would also say they know what they’re doing when it comes to this,” Zaino said.

Rep. Dan Troy (D-Willowick) told Zaino he agrees emergency levies are creating an issue.

“They are problematic to me. I have one school district, I think about 50 percent of their millage is emergency levies,” Troy said. “I ask questions like, ‘Is there a point where the emergency ends?’ … The response I get is, ‘Dan, what do you have against the kids?’”

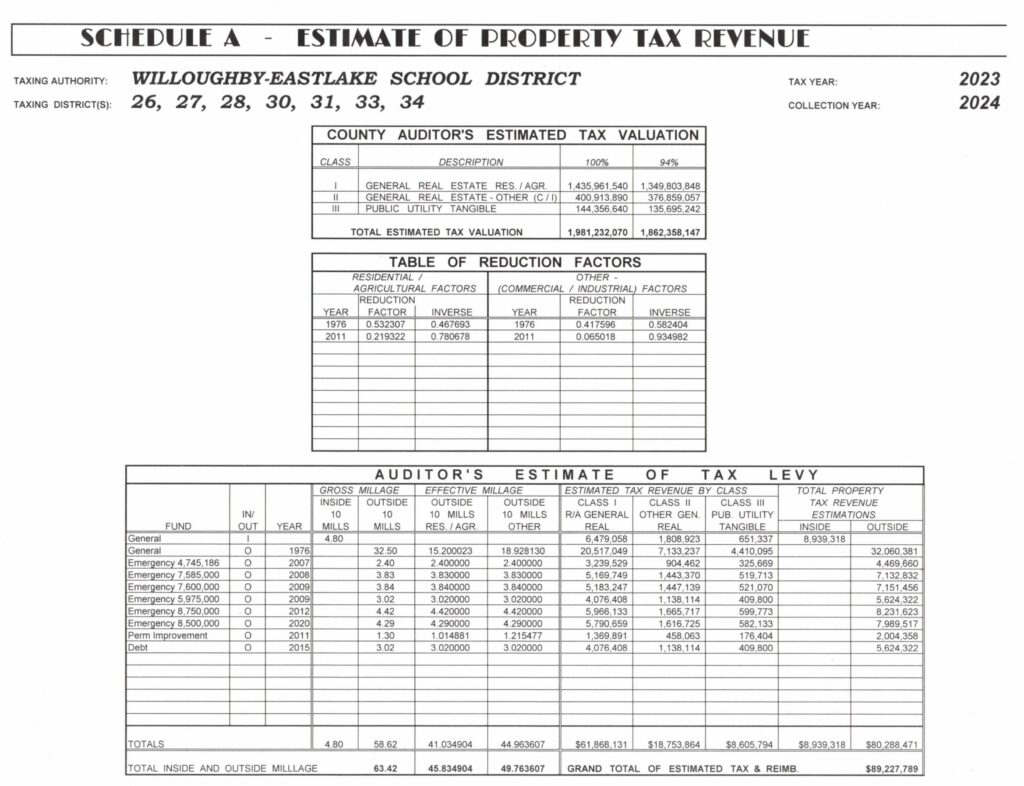

LFC Input: Representative Troy is referring to the Willoughby-Eastlake School District. Here is the Auditor’s Schedule A detailing all of the levies for the district:

There are six “emergency levies” used by the School’s Administration and the School Board to dupe the taxpayers. Emergency levies are not subject to the impact of HB 920. The total tax (at a 94% collection rate) collected annually for the “emergencies levies” is $40,599,410, which is 45.5% of the $89,227,789 taxes collected.

The Willoughby Eastlake inside millage of 4.80 mills is added to the effective tax rate of the General Outside Millage levy of 15.2 mills to arrive at the 20-mill floor. So they benefitted over the years from the emergency levies not being impacted by the HB 920, and now reap the windfall from the unconstitutional 20 mill-floor.

Troy also suggested state revenue reductions have contributed to property tax woes by shifting expenses for services like children services and developmental disabilities systems to the local level.

“In many cases, what used to be 75 percent funded by the state is now being 80 percent funded by property taxes in some of these areas,” Troy said.

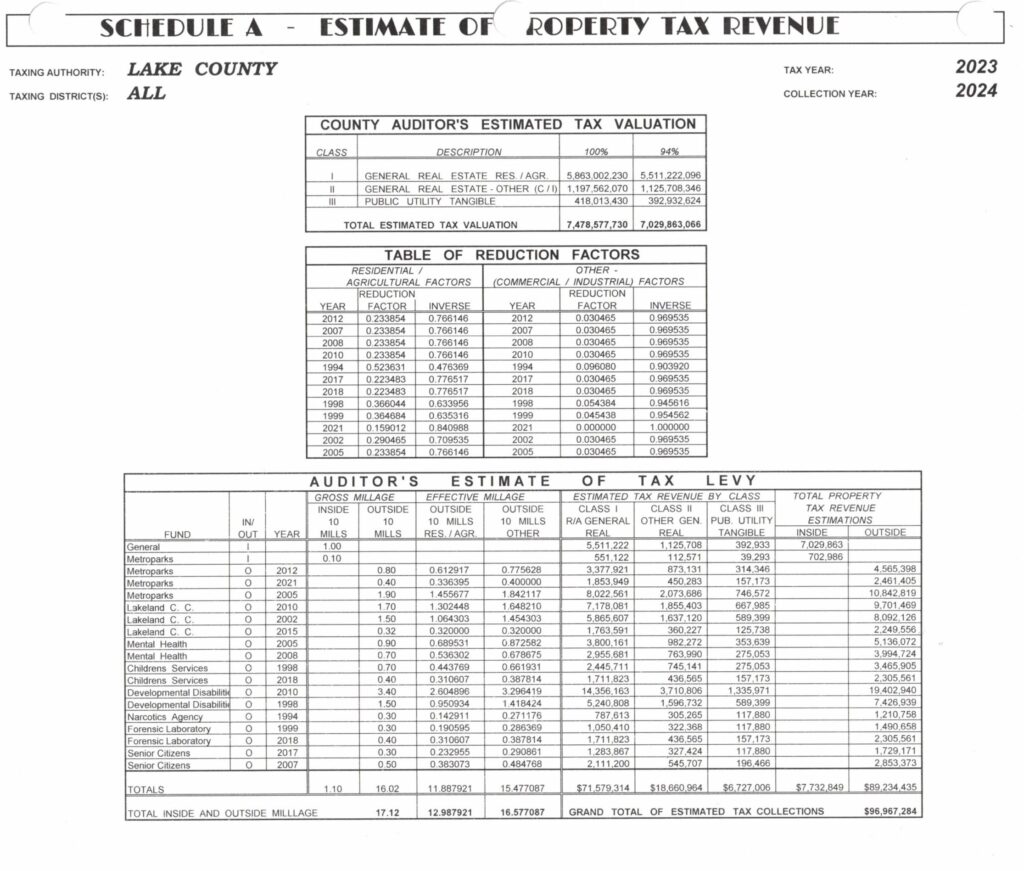

Here is the Auditor’s Schedule A covering the County’s taxing authorities.

The Children’s Services are collecting $5,771,466 and the Developmental Disabilities (Deepwood) is collecting $26,829,879 annually from the Lake County taxpayers. The State has shifted the burden to the local taxpayers.

To add insult to injury the Lake County Budget Commission, allegedly the “watchdog” for the taxpayers guarding against the collection of excessive taxation, has been relegated to a “rubber stamp” for the taxing authorities. This, in part, is due to a ruling by the Lake County Prosecutor, Charles Coulson, preventing the Budget Commissioner from lowering the taxes collected due to excessive cash reserves.

This has allowed massive accumulation by many of the taxing authorities. For example, Deepwood has $65 million in cash reserves, Crime Lab $7 million, Lake Metroparks $30 million.

The $20 million that the Lakeland Community College receives annually from the taxpayers keeps them from being in State receivership for their horrible mismanagement of taxpayers’ funding. Hopefully, the new board can put the college on the correct path to financial stability. However, if they continue to believe that Diversity, Inclusion and Equity is the cornerstone of their institution then they will continue to flounder.

The estimated 30% increase in Lake County property values will mean a windfall for those school districts at or near the 20-mill floor. Riverside will get $3.6 million, and Willoughby-Eastlake will get $8.0 million without a vote of the taxpayers.

Blessing asked Zaino about the prospect of financing property tax relief by eliminating some of the other carveouts in the tax code.

“How do you feel about the idea of paying for that with some of the massive pile of money we spend on our tax expenditures?” Blessing asked. “For the 11 years that I’ve been here, despite screaming about these left and right, they just keep ratcheting up.”

“When you look at those carveouts … a lot of them you have to have,” Zaino replied. “They’re constitutional problems, they’re competitive problems that are necessary. That’s where the real money is, the big money. But there are little things here and there.”

He said he generally does advocate for policymakers to pursue broad-based, low-rate tax structures, arguing lawmakers for the most part have honored that principle since creating the Commercial Activity Tax (CAT) about 20 years ago to replace the Corporate Franchise Tax, “which was a sieve.”

Rep. Bride Sweeney (D-Cleveland) said she’s hesitant to address issues with the 20-mill floor when Ohio is only now addressing the overreliance on local property taxes for schools with the phase-in of the Cupp-Patterson formula, aka the Fair School Funding Plan.

LFC Comments: The 20-mill floor legislation is, in our opinion, unconstitutional because it violates Article XII, Section 2 of the Ohio Constitution by treating the outside millage as if it were inside millage.

HB 920, meant to eliminate the impact of rising home values by reducing the outside millage rate to an effective rate, stops when the inside millage and outside millage collected reaches 20 mills.

The outside millage is treated like inside millage, and property taxes skyrocket without a vote of the taxpayers. There is an old saying: “If it walks and quacks like a duck, it’s a duck”.

If the outside millage is treated like inside millage – it’s inside millage, and is in excess of the 10 mill limit mandated by the Ohio Constitution and codified in the Ohio Revised Code.

Also, property taxes are charged based on unrealized gains in property values. For example, if you build your house 20 years ago for $100,000, but it is now valued at $300,000, then you are paying property taxes based on an unrealized gain of $200,000. You will only realize the gain when you sell your property.

Another deception not told to the taxpayers is the cost to administer the property taxes. The only question we have is how many $Billions are paid by the counties and State to administer the immoral property tax. A sales tax is a much more cost effective way of collecting taxes.

“To pull the rug from under these districts at this moment could actually have worsening effects,” she said, noting many districts on the 20-mill floor are rural or Appalachian and generate a paltry amount of money with each mill. “I just think that’s the missing piece, we have to understand the state has failed.”

The committee also heard Wednesday an overview of property tax systems across state and local jurisdictions in the U.S. from the National Conference of State Legislatures’ (NCSL) Eric Syverson, and about the Council on State Taxation’s (COST) property tax scorecard from COST’s Fred Nicely.

Syverson said Ohio is in line with other states in terms of the share of revenue derived from property taxes, but above average in how much education funding comes from local property taxes.

Rep. Tom Young (R-Centerville) asked if the number of jurisdictions able to levy property taxes is an issue for Ohio.

“Do you feel the menu of taxation, all the jurisdictions – does that play a huge role in this quagmire we’re in here in Ohio?” Young asked.

“Ostensibly, Ohio is definitely on one end of the spectrum with a lot” of taxing jurisdictions, Syverson said.

Troy asked if local governments generally get reimbursed when states enact property tax relief. Syverson said typically they don’t, but it is more likely when the relief is targeted to seniors or veterans.

Nicely noted Ohio received a D on COST’s property tax scorecard; the largest number of states get a C, and none an A. Subscores for Ohio included a D in the transparency category, C in the consistency category and D in the procedural fairness category.

Nicely said property tax reform is a hot topic in legislatures across the U.S. While COST would typically track about 50 pending bills in a given year, the volume of tracked bills more than doubled in the past year.

Rep. Tracy Richardson (R-Marysville) asked Nicely about “tried and true” property tax procedures Ohio should consider. Nicely said calculating taxes based on the full market value of a property, rather than just a portion of the assessed value, would make the system more understandable for taxpayers.

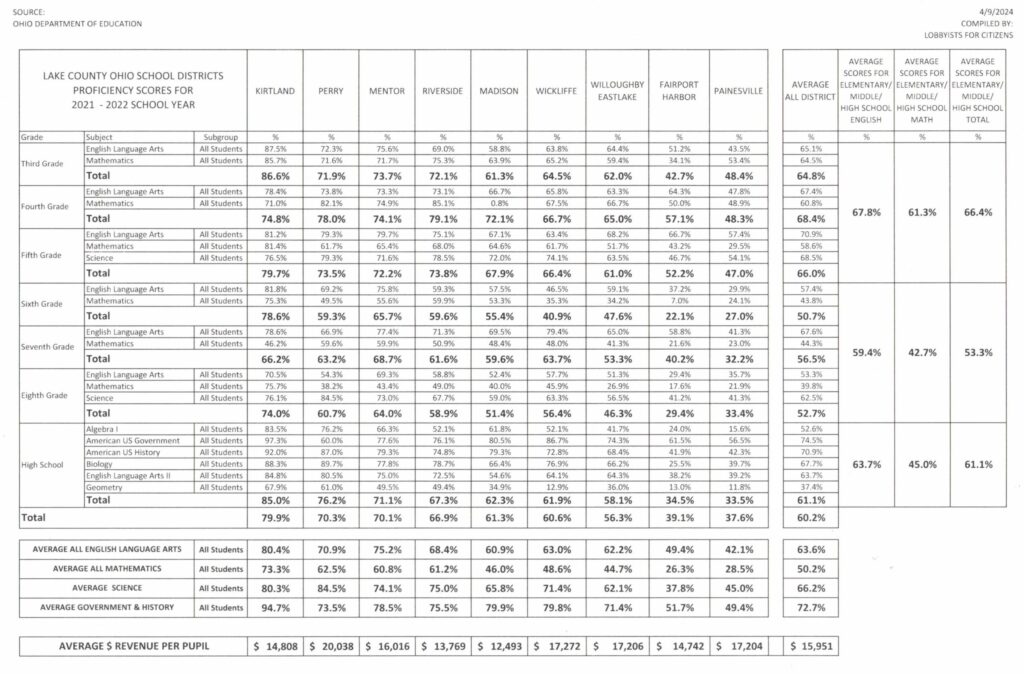

LFC Comments: So how are the Lake County School districts doing with all the property taxes that they are getting? Here is a schedule of the proficiency scores for all districts for the school year 2021 – 2022.

When Representative Troy questioned the validity of the “emergency levies” the response he got was: “Dan, what do you have against the kids?”. After reading these proficiency scores, with Kirtland being the exception, we have to ask the school administrators and school boards: “What do you have against the kids?”

Mathematics is now a foreign language to most of the children.

Categories: Contributors, Lake County - General, Uncategorized