In our ongoing efforts to better understand the very complex world of property taxes, we did some research on how the State and the Lake County Auditor’s offices work together to appraise, and assess our residential property values in order to determine our real estate taxes. We would like to thank the Lake County Auditor Chris Galloway, the Chief Deputy of Real Estate Scott Yamamoto, Barbara Hogya, Lake County Auditor’s premier property tax expert, and Shelley Wilson of the State of Ohio Tax Equalization Board for their invaluable help with this project.

*********************1776

Let’s start with what gives the State and the Lake County Auditor the authority to collect property taxes.

- The Ohio Revised Code Section 5709.01 (A) states that “all real property in this state is subject to taxation, except only such as is expressly exempted therefrom.”

- The Ohio Revised Code section 5713.01 states that “each county shall be the unit for assessing real estate for taxation purposes. The county auditor shall be the assessor of all the real estate in the auditor’s county for purposes of taxation…”

- The Ohio Revised Code Section 5712.03 states that “the county auditor, from the best sources of information available, shall determine, as nearly as practicable, the TRUE VALUE of the fee simple estate. [LFC Comment: Fee Simple Estate means absolute ownership of the land]

What does “true value” mean?

- “The auditor shall determine the taxable value of all real property by reducing its true or current agricultural use value by the percentage ordered by the State of Ohio commissioners.

- In determining the true value of any tract, lot, or parcel of real estate under this section, if such tract, lot, or parcel has been the subject of an arm’s length sale between a willing seller and a willing buyer within a reasonable length of time, either before or after the tax lien date, the auditor may consider the sale price of such tract, lot, or parcel to be the true value for taxation purposes.”

- The arm’s-length principle of transfer pricing requires that the amount charged for a house is the same for transactions between strangers as it is for transactions between those with personal ties. this protects one or more parties from being manipulated by an inflated market value.

- There was an Ohio Supreme Court ruling that stated “the best evidence of the true value in money of real property is an actual, recent sale of the property in an arm’s length transaction.”

What is a Real Property Conveyance Fee Statement of Value and Receipt?

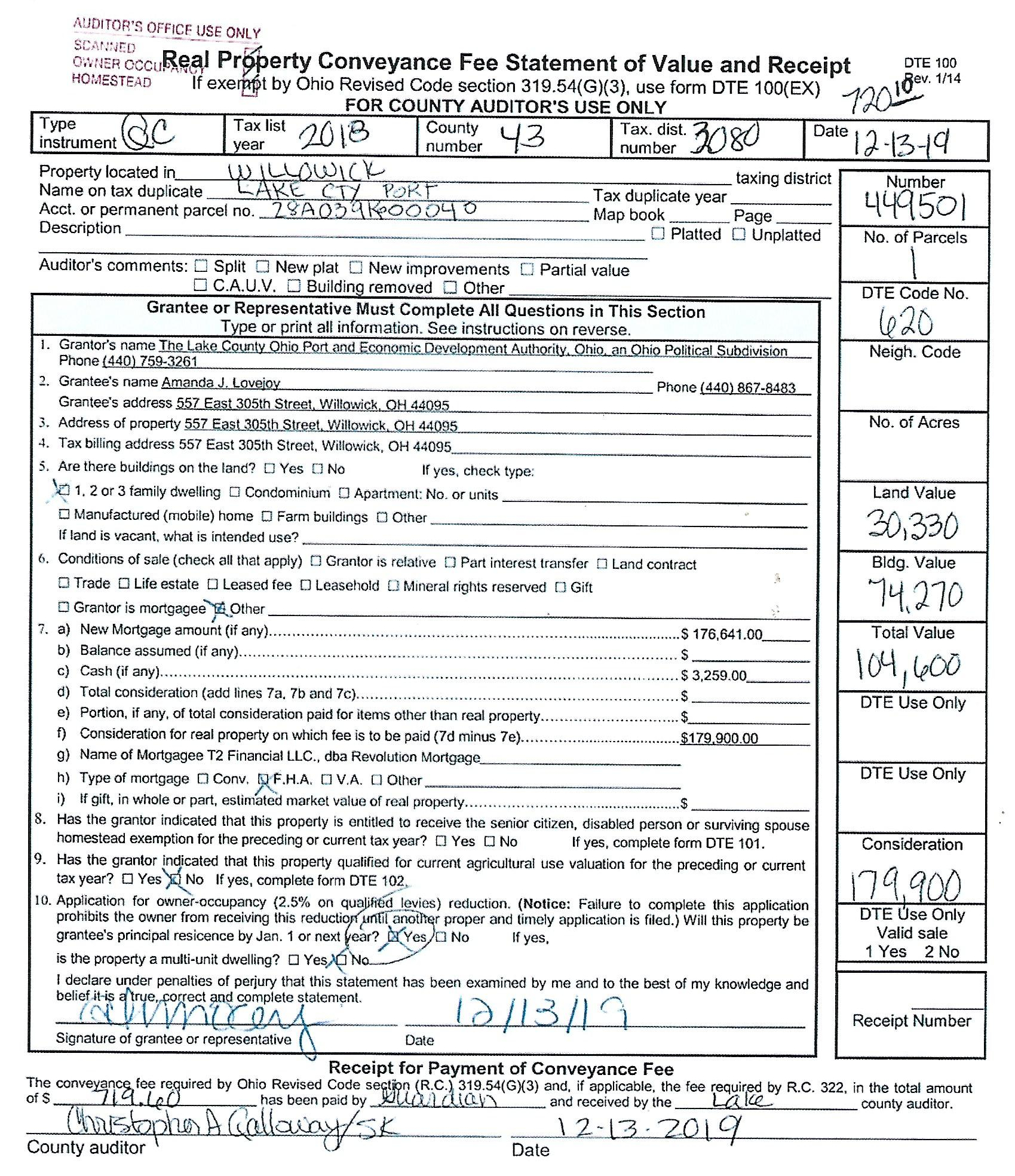

This is the main document that is a basis of the reappraisals. We were told that every parcel of land in the State that has been sold has this form on file with the State of Ohio. The Lake County Auditor’s office tracks the ~109,000 parcels in the County, and handles ~11,000 sales every year. Here is an example of the Conveyance Statement for the ‘Better Flip‘ home in Willowick:

The two important numbers for our research are the ‘Total Value‘ [$104,600], and the ‘Consideration‘ [$179,900]. The ‘Total Value‘ represents the current appraised value that the Auditor’s office has on file for the property. The ‘Consideration‘ is the sale price for the property. In this case, the arm’s length transaction is between the new homeowner and the Lake County Port Authority. When we divide the ‘Total Value‘ by the ‘Consideration‘ for the ‘Better Flip‘ home, the percentage is 58.1% [$104,600 / $179,900]. This tells us that the Lake County Auditor has the ‘Better Flip’ home currently appraised at 58.1% of the selling price. However, before the three year appraisal adjustment in 2021, this parcel will be reappraised, and the 58.1% should be increased. The new percentage is unknown at this time.

Why is this percentage important?

The State of Ohio uses an organization known as the International Association of Assessing Officers (IAAO) to help determine proper valuation techniques, and establish standards to ensure that properties are not over-valued or under-valued, thereby causing incorrect appraisal values. Here is their website link: https://www.iaao.org/wcm/About/wcm/About_Us_Content/About_Home.aspx?hkey=a67eedbd-8c6d-4711-ad95-02b41865aaa0

From their website, we learn who they are, and what they are all about:

“IAAO is a nonprofit, educational, and research association. It is a professional membership organization of government assessment officials and others interested in the administration of the property tax. IAAO was founded in 1934, and now has a membership of more than 8,000 members worldwide from governmental, business, and academic communities.”

The IAAO suggests that the ‘Appraisal to Consideration’ percentage should be in the range of 90% – 110%. The State of Ohio uses the range of 92% – 94% because they try not to overvalue the parcels.

In our ‘Better Flip’ example, with a sale price (Consideration) of $179,900, the State suggests that the appraised value for the taxation calculation should be $165,508 – $169,106. [$179,900 x 92% or x 94%]. It will be interesting to see where the Lake County Board of Revisions sets the appraised price for the ‘Better Flip’ home.

The appraised value of the parcel listed on the Real Estate Tax Bill is supposed to represent the current market value of the property,.. However, if you are interested in selling your property that amount is not necessarily what your selling price will be.

Not to further complicate things, but you must understand that the Ohio Revised Code mandates that the appraised value is multiplied by 35% to arrive at the ‘assessed value’. On your property tax bill it shows assessed value as 35% of “market”. Market and appraised value are one in the same for the purposes of your tax bill.

The ‘assessed value’ is then multiplied by the inside millage rate , and the effective tax rates for the outside millage. The inside millage is set at a maximum of 10 mils by the Ohio Revised Code, is not voted on by the taxpayers; we may see automatic property tax increases when the appraised values increase because of revaluations by the Auditor’s office.

We are planning another article to explain inside millage. Currently, it is set at 8.9 mills and the ability to collect the remaining 1.1 mills is controlled by the Lake County Commissioners.

We hope we have not lost anyone yet, but it gets even more complicated…so hang in there. We will do our best to simplify things.

How often are properties reappraised?

A general reappraisal is required by Ohio Law every six years (Sexennial Appraisal), and an update every three years (Triannual Update). Every six years the State mandates that the exterior of each parcel be viewed so that a correct property appraisal is made. However, the three year assessment update is done by the County Auditor’s office mainly by using statistics generated by the State and the County’s Board of Revisions department.

The State summarizes all of their “Conveyance” forms accumulated for the last three years. [Remember, they get copies of all real estate sales in the State] The summary of all the “Conveyance” statements determines if there has been an increase or decrease in real estate values for each municipality and County in the State. For example, if their records show that Willowick’s or Lake County’s recent sales indicate that the existing home appraised values is only 88% of the current sales prices, they would suggest a overall County increase of 4% – 6% to arrive at their pre-determined 92% – 94% optimum Appraised to Sales Price ratio.

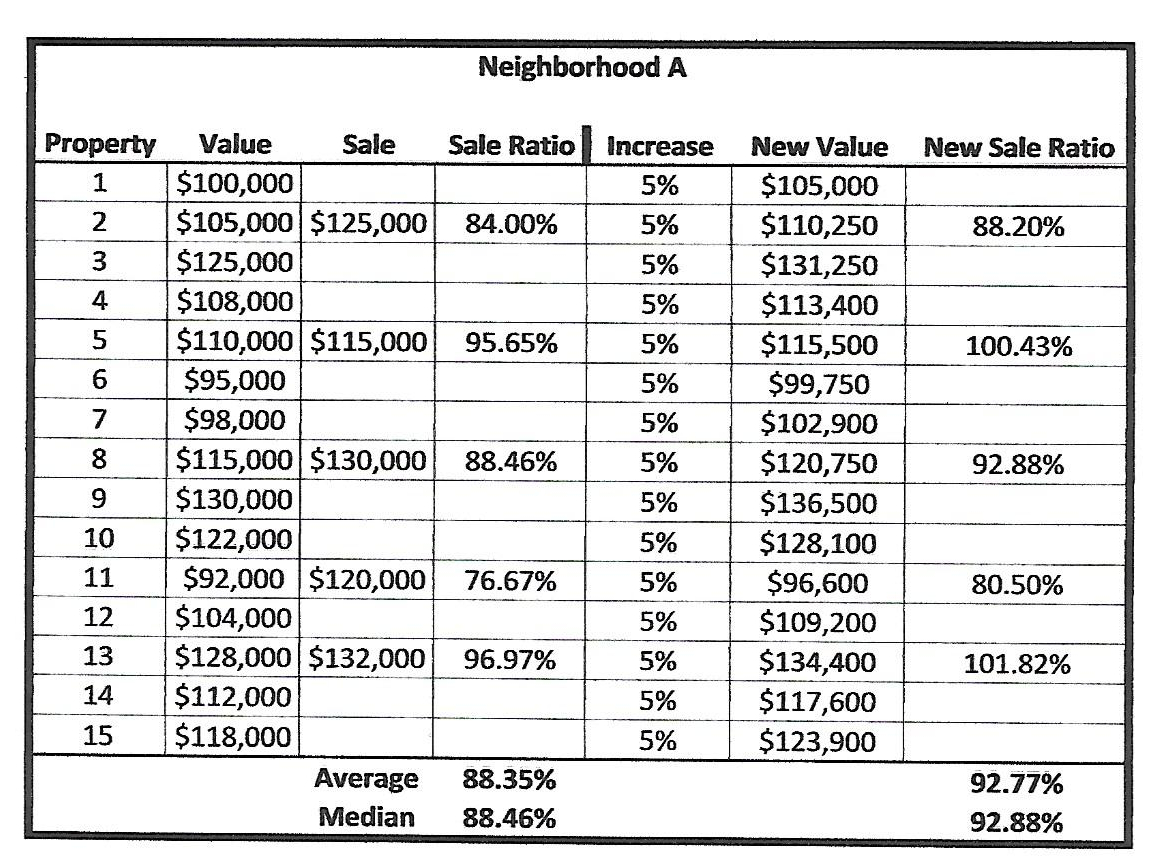

The County Auditor then will review the ‘Appraised to Sales Price’ ratio for each taxing district and then by “Neighborhood”. There are over 700 “Neighborhoods” in the Auditor’s database. Here is an example, provided to us by the Auditor’s office, of some of the statistical analysis that they do to adjust the appraised value of the homes:

Auditor’s Example of a Neighborhood

In this example, it was determined that an overall 5% increase in the appraised values was required to achieve the State’s desired 92% – 94% ‘Appraised to Sales Price’ ratio. Please note that this may cause some homes to have an appraised value greater than the selling price!

If the homeowner detects that their appraised value is greater that the purchase price (see property #5 and #13), the homeowner must file with the Lake County Board of Revisions to get their appraisal value reduced. IT DOES NOT HAPPEN AUTOMATICALLY!

We were told that if there are any new sales that seem to be a deviation from the other property values, individual decisions are made on those sales,. Any deviations outside of the statistical range may be excluded. [The ‘Better Flip’ home is an example]

Each neighborhood’s property valuation may increase or decrease based on sales within the past 3 years. However, the objective is to have the overall County property valuations equal to the percentage increase or decrease mandated by the State, and still stay within the 92% – 94% range.

What is the impact of a ‘Better Flip’ home on a neighborhood?

The ‘Better Flip’ current appraised value of $104,600 would be reviewed, and probably increased in value based on the additions, or modifications to the home. We have been told that the BOR does not just take a flat 92% – 94% calculations of the $179,900 sales price. The homeowner would be paying the increased property taxes before the parcel of land is included in the “Neighborhood” calculations for the 3 year reappraisal. To reiterate, we have also been told that if a home appraised value, or sale price in a neighborhood is an anomaly (a deviation from the norm of the neighborhood) then that parcel may be excluded from the calculation for the neighborhood increase or decrease.

If the ‘Better Flip’ house is not excluded there is a good chance that the neighborhood would experience a property tax increase.

In conclusion:

Hopefully, we have provided some insight into the complex world of property taxes. We would like to see the whole process simplified so that the average homeowner has a chance to understand their property tax statement. Our current property tax law has evolved into a tangled web that is far too complex for the taxpayers and the employees that are paid to implement the property tax laws.

For example, we would like to see the entire concept of “millage” be replaced by a percentage of appraised value. We would also like to see the property tax reduced or replaced by another form of taxation – probably an increase in the state sales tax.

We would also like to see property tax ballot language be made more understandable for the voter. It is too bad that the current State Representative, and current candidate for Lake County Commissioner John Rogers, does not share that view. Mr Rogers is also the current Executive Director of the Lake County Land Bank. It is a quasi governmental entity that handles all the foreclosed properties in Lake County. Why do you think that Mr. Rogers does not want the taxpayers to understand the property tax ballot language. Makes one go….HMMMM?

The Lake County taxpayers can rest assured that we have some very competent people in the Board of Revision department of the Auditor’s office. We may not like property taxes, but it is comforting to know that the people responsible for following and executing the Ohio Revised Code sections dealing with property taxes do it very well.

Categories: Real Estate Taxes, Uncategorized

Leave a Reply

You must be logged in to post a comment.