We have spent a great deal of time analyzing the property taxes associated with the Lake County Financing District levy. Our goal is to provide the facts that will help Riverside School District taxpayers decide whether or not to support the tax levy on the March 17th ballot. Riverside school officials have been very transparent in providing any and all documents to help with this article.

The Riverside School District website does a good job of explaining the who, what, why and where questions concerning the levy. However, they fail to really show the complete impact on the taxpayers of the Riverside School District. That is our goal in this article.

http://www.riversidelocalschools.com/protected/ArticleView.aspx?iid=6G202PY&dasi=3U30

From their website we learn the following:

Q. What is a county school financing district?

“A county school financing district is a group of independent local school districts that agree to pool their valuation and request a levy to support specified educational programs across the entire group of districts.”

Q. Which districts participate in the Lake County School Financing District?

“The Lake County School Financing District consists of Madison, Painesville City, Perry, and Riverside local school districts. The ESC of the Western Reserve (formerly known as the Lake County Educational Service Center) is the taxing authority, which collects the tax proceeds and distributes them to each of the four school districts based on an agreed upon formula.” [LFC Comment: The officials from the four school districts agree on the distribution formula every five years.]

Q. How Is the money from the levy distributed?

“The member districts currently receive the majority of their share based on a proportionate share of each district’s total enrollment. If the levy is renewed, the proceeds will be distributed based on each member district’s proportionate share of tax valuation.” [LFC Comments: This is a very important factor, and it’s impact will become obvious when we show you the numbers. Although Class I and II revenue are distributed based on enrollment, Class III distribution is split: 2/3 based on enrollment and 1/3 based on each district’s Class 3 valuation]

Here is Riverside’s Powerpoint presentation about the levy: Treasurer Update – Financing District – October 2019

(Sorry, you will need Powerpoint software to see it)

It does a very good job of explaining the details of the levy.

From the Powerpoint presentation, we recreated the property valuation chart detailing the valuation history of all three classes from 2010 – 2018. You can see that both Class II and III valuations have decreased significantly while Class 1 (Residential / Agricultural) has increased since 2010. RIVERSIDE PROPERTY TAX VALUATIONS

Unfortunately, we could not get the valuations from the year the levy started – 1990. They are buried in the basement of the County Administration building.

UPDATE: 2/13/20:

We were able to get the tax collected for the tax year 2000 from the Auditor’s office. Here is a schedule of the property taxes collected comparing 2000 versus 2019. We can clearly see the drop in revenue from the Perry School district due to the drop in valuation of the Perry Nuclear Plant. It appears the the Riverside School District has been subsidizing the Painesville School District for quite some time.

LFC Analysis – What does this all mean to the taxpayers?

To get directly to the heart of the matter, here is our summary of what has happened over the years:

- The District was initially formed to distribute the excessive property taxes collected from the Nuclear Power Plant in 1990 over the four school districts. (Madison / Perry / Painesville City / Riverside) The property tax was also collected on Class I and Class II properties from all four districts. Class I property was subject to HB 920, but Class II and Class III were taxed at the full 4.90 mills.

- The total tax fund was split among the four school districts based largely on enrollment. However, Class III was a split of 2/3 on enrollment, and 1/3 on tax valuation.

- With the subsequent devaluation of the power plant since 1990, there has been a shift in the tax burden from the Class III property to the Class I (Residential / Agricultural) and Class II (Commercial and Industrial). The increasing residential property tax base in the Riverside School District, due to more development and rising valuations of existing homes, started to play a more significant role, although HB 920 was reducing the effective tax rate.

- The total property valuation of the Riverside School District is $1,117,894,360 (54.7% of the total Financing District’s $2,042,411,180. Painesville School District property valuation is $185,623,590 (9.0% of total Financing District). From the State of Ohio Cupp reports we determined that Painesville and Riverside average daily enrollment were almost identical – 3,848 for Painesville and 3,877 for Riverside in 2018.

- Since the distribution of the taxes collected was based on enrollment, the taxpayers in the Riverside School District have been subsidizing the Painesville and Madison school districts for many years. It is difficult to quote an exact amount, but our estimate is that it has been in the range of $600,000 – $700,000 per year. It has been the basic governmental redistribution of the wealth without the taxpayers having a clue that it has been happening.

- All four school districts meet to decide how to allocate the tax revenue every 5 years. The Riverside school officials realized the inequities of the distribution based on enrollment. There is now an agreement to distribute the funds based on the property tax valuation of each district. This will result in the property taxes previously going to the other districts to remain with the Riverside School District.

- LFC contends that the original intent of the Financing District is no longer valid; we now have just a conventional operating levy, but are needlessly spending money with the Educational Service Center doing the bookkeeping for the whole district.

- However, there are a couple of reasons to maintain the existing levy.

-This levy still has the two rollback credits totaling 12.5% from the State of Ohio. (worth approximately $150,000 – $200,000 annually)

– The tax collected from the Riverside School District taxpayers (~$600,000 each year) will go to the Riverside school district rather than Painesville and Madison schools.

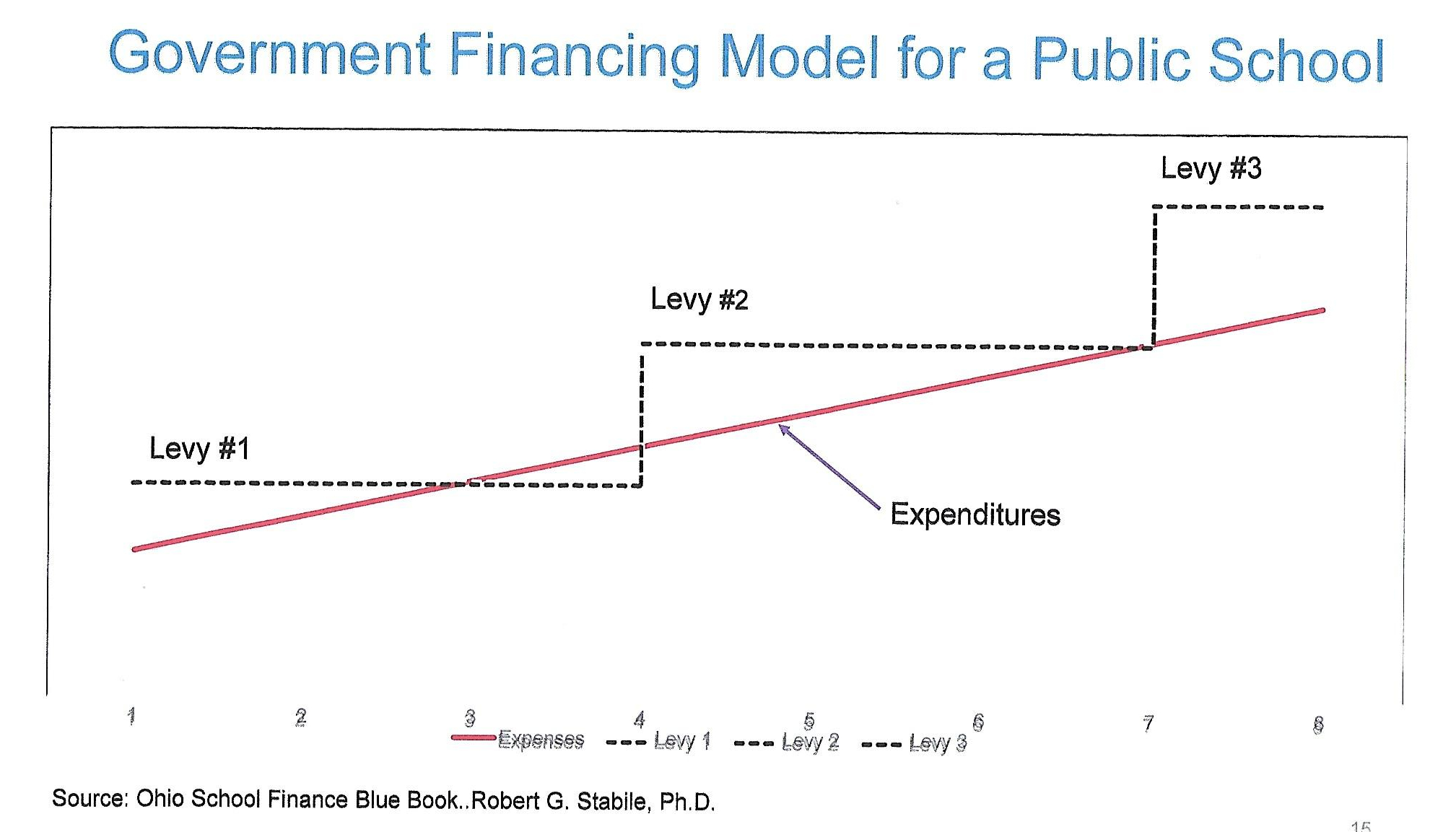

LFC is very concerned that the current method of public school funding is not sustainable. The operating expenses of schools will NEVER go down. The Riverside schools teachers’ salary and benefits are projected to grow at rate of over 4.6% per year. However, most seniors and those living on fixed incomes are not realizing that level of growth in their annual income; they are being taxed out of their homes that they have worked all their lives to achieve. Here is a graph illustrating what is happening with public schools finances. Expenditures will NEVER go down, and requires a new property tax levy every 3 -5 years. This graph is a recreation of a graph created by Dr. Robert G. Stabile, Ph.D. in his book titled Ohio School Finance Blue Book.

However, when you add the housing affordability threshold to the graph, you can see that eventually the ever-increasing property taxes will ultimately price seniors and those on fixed incomes out of their homes. This graph was created by LFC.

THE CURRENT METHOD OF PUBLIC SCHOOL FUNDING IS NOT SUSTAINABLE AND UNCONSTITUTIONAL!

*********************1776

The balance of this article will give you the details that we used to provide the summary above. It is really getting “into the weeds”, but at least you can check our work.

Here is the Auditor’s summary combining all of the taxing districts that make up the Financing District (Note the taxing districts at the top of the page):

Lake County Financing District Summary 2019 – 2020

Here is the Madison School District (Taxing Districts 1, 2 – Madison Township and Madison Village):

Madison School District 1 and 2

Here is the Perry Local School District (Taxing Districts 3, 4, 5 – Perry Township, Perry Village and North Perry Village):

Perry School District 3 4 5

Here is the Riverside Local School District (Taxing Districts 7, 8, 11, 13, 35 – Leroy Township, Concord Township/Painesville, Painesville Township, Grand River Village, Painesville City/Painesville Township)

Riverside School District 7 8 11 13 35

Here is the Painesville City Local School District (Taxing District 15 – Painesville City)

Painesville School District 15

From all of this raw data we created the following schedules:

The first schedule summarizes the property tax valuation and estimated property taxes to be collected by taxing district. The numbers highlighted in yellow ties out to the total on the Auditor’s schedule A reported above.

- The 96% column is the Auditor’s way of accounting for property tax not being paid, although the millage rate reported to the taxpayer is always based on the 100% valuation. The actual receipts will vary based on the collections.

- The original goal of the Financing District was to share the tax collected from the Perry Nuclear Power Plant. However, the declining valuation of the plant has shifted the tax burden from the Class III public utility column to the Class I Residential / Agriculture and Class II Commercial and Industrial. The Class 1 taxpayers are paying 63.1% of the taxes.

Back in September, 2019, we wrote about the Lake County School Financing District. In this article, we provided the distribution of the 2018 revenue collected for this District. The information was given to us by the Treasurer of Lake and Geauga County Educational Service Center, who maintains the financial records for the Financing District.

https://lobbyistsforcitizens.com/2019/08/19/lake-county-financing-district-are-you-ready-to-cry-uncle/

Our final schedule uses the data from the Auditor’s Schedule A and compares it to the information given to us by the Educational Service Center accountant. We wanted to determine how much was being collected from each taxing district versus how much each school district received by the pre-approved method (based on enrollment) of allocation.

Although we are comparing 2019 tax year with 2018 payments, it still represents what is happening with the tax revenue. So what are the numbers telling us?

- The property taxes collected in 2018 were greater than anticipated. This may be due to shortfalls of payments in prior years, and through collection efforts more property taxes were collected.

- Approximately $92,000 was paid in various expenses. The Auditor and Treasurer fees would remain if we had a separate operating levy.

- The big take-away is that the taxpayers in the Riverside School District, and to a lesser degree Perry taxpayers, are having their taxes fund the Painesville and Madison school districts! We wonder how long has this been happening, and how many actual dollars have been shifted without the knowledge of the taxpayers?

- What does this mean for the residential taxpayers in the Riverside School District? Currently, they are paying an effective tax rate of 2.2277084 mills. The original millage was 4.9, but the impact of H.B. 920 reduced it to 2.2277084. However, the State of Ohio provide two credits totaling 12.5%. So the net effective tax rate is 1.93552 (2.2277084 x 85%). This translates to $67.74 per $100,000 of home valuation. ($35.00 x 2.2277084)

- In 2018, according to the CFO, the Riverside school district received $2,199,647.61 from the Financing District levy. With the aid of the Auditor’s office, we have determined that to collect that much revenue with a new operating levy we would need to collect ~1.967 mills. [$1,117,894,360 total property valuation x 1.967 mills / 1,000 = $2,199,647.61] However, a new levy loses the 12.5% State Rollback credits, and taxes all classes of property at the same millage. This is also giving a tax break to business and the public utilities, and the expense of residential customers.

Categories: Lake, Real Estate Taxes

Leave a Reply

You must be logged in to post a comment.